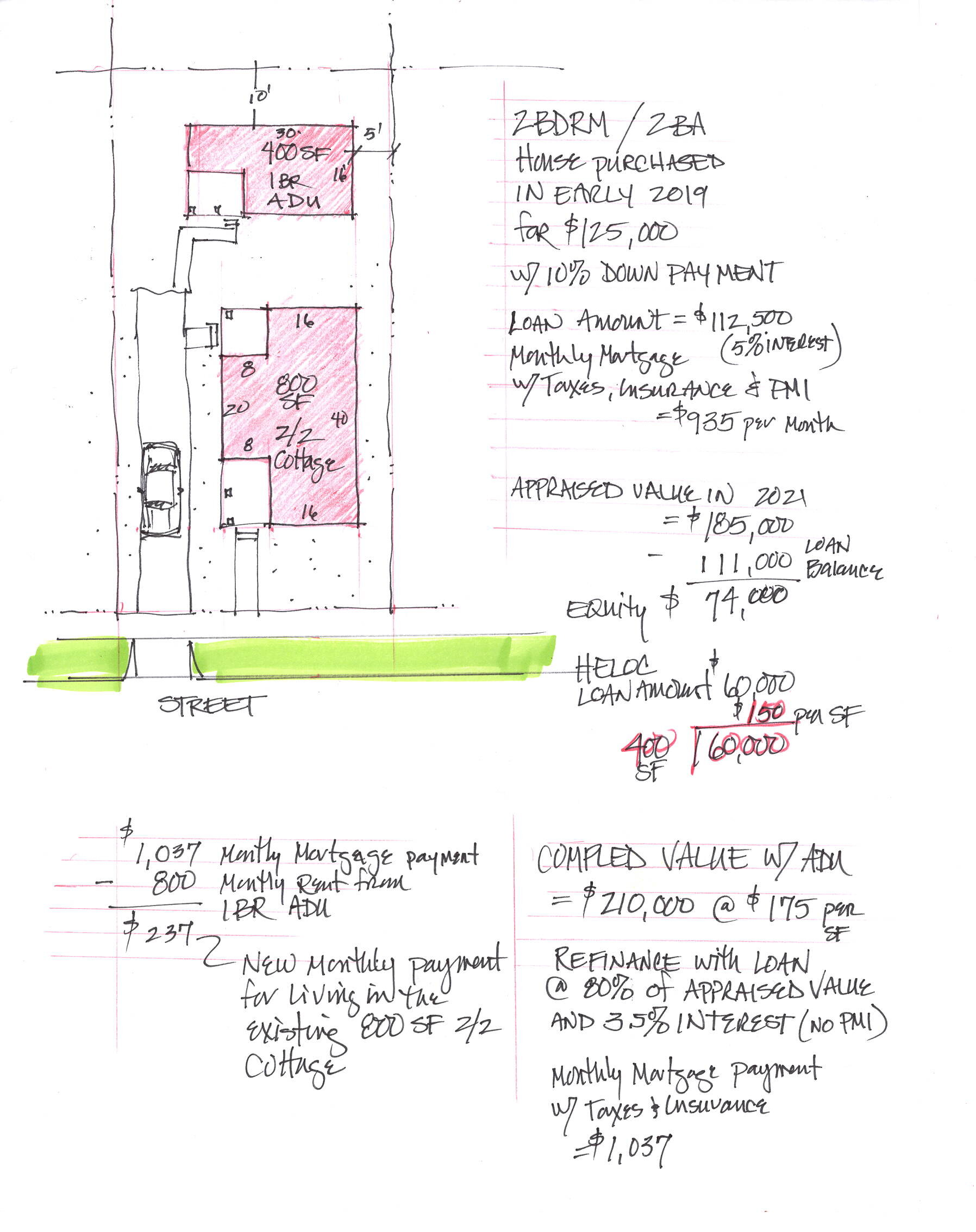

Ivy with 8 gallon stock pot for scale

Here is a guest blog post from one of my favorite humans. Ivy Van is a what many would describe as “a handful”. She is a small developer in New Hampshire just completing the conversion of a former bed and breakfast into a tri-plex. She is the chair of her local planning board and serves in the State Legislature. She is a recovering daily newspaper reporter, elementary school teacher, and driving force behind her village’s Community Dinner. She is currently working with the Congress for the New Urbanism’s Project for Code Reform. I think she is a mensch, —in spite of her questionable decision to quote me in the beginning of this piece. Here’s Ivy Vann:

“People tend to think that building and real estate are a mysterious black box. Specifically a Mysterious Black Box full of money and jerks. If how money is made building and operating buildings is mysterious it is so easy to identify the builder, developer, or the landlord as the "Other" and then proceed to question their character, motivation, and business practices.

We don't have empathy for someone alien to our experience. Once we vilify them or hear about what a bad person they are by virtue of their line of work, we are not inclined to get to know them or acquire any empathy or understanding of their reality.

While building and housing math is certainly relentless and unforgiving, some folks figure the best solutions will come from someone else's pocketbook.”

R. John Anderson

People make some fancy shoes, other people spend a lot of money on them, but I don't think I've ever heard anyone complain about the shoe store or the shoe manufacturer making a profit. People build some houses, sell them, maybe make a little money, and everybody complains that they're making money, that they're greedy, they're only in it for themselves.

Why is it okay for the shoe manufacturer to make money but not okay for the builder to make money?

You can argue that building houses is a riskier business and that the builder should maybe make a little more money because of taking that risk rather than blaming them for earning a living.

"It's all about the money," people say.

Yeah, it is about the money. It's about buying a piece of land, borrowing money to build a building, carrying the interest until you can sell the house, hoping that you can sell it for what you put into it, hoping that steel prices don't go up, and that there isn't a hurricane that pulls all the carpenters away from your job, hoping the weather lets you finish on time so you don't lose your shirt.

I know a lot of builders and I don't know even one that hasn't gone bust at least once. There is real risk involved. And people deserve fair compensation for their time and talent and risk.

Towns don't get to tell builders that they have to build things that are not going to make at least some money. We can't demand that builders take a loss to produce what we would like to have built. We can structure our regulations so that we have a fighting chance of getting something that doesn't make our place worse, but we can't demand something that a builder can't deliver in today's economic world.

We have to do the math, both from the builder's perspective and from the town's perspective.

Brand new single-family houses which cost $200 a square foot to build are never going to be affordable on an entry-level salary. Let's work to make other housing choices readily available so that more people have a chance to live here.

New houses on two acre lots on new streets will never pay enough in taxes to cover their services.

Let's use the infrastructure we already have when possible so we don't create more expenses for the town.